Is There a (Profitable) Future for Acquiring?

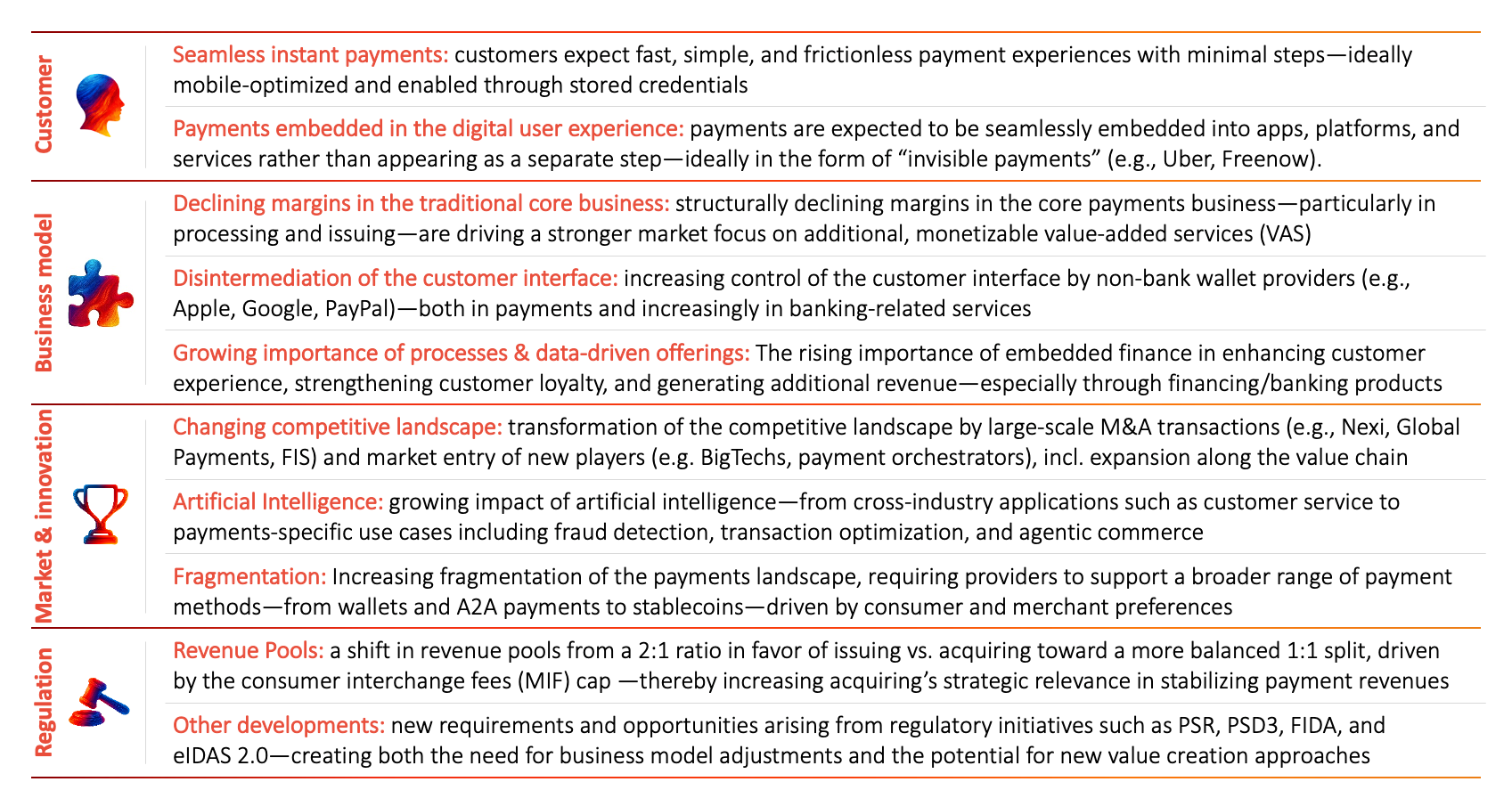

Why the acquiring business remains relevant, how the future winning model works, and why banks are asking the wrong question. The payments market is undergoing a fundamental transformation: digital transaction volumes continue to rise, new competitors are offering bank-like products, and innovative solutions are changing customer behavior (see Figure 1 for more details on key trends). Against this backdrop, traditional business models are increasingly coming under (margin) pressure and facing growing strategic pressure to act. The discussion often focuses on the issuing side: Which wallet should be offered? Who controls the customer interface? What role will cards play in next-generation payment offerings? By contrast, the acceptance side often receives less attention. Yet acquiring manages the acceptance of digital payments on the merchant side — from transaction authorization to settlement. It represents the central interface to the real economy where acquirers and PSPs orchestrate revenue streams, access valuable transaction data, and maintain direct merchant relationships, making the business a strategic entry point for new financial products. In this article, we address a question that decision-makers — particularly in banks — have repeatedly raised with us: does acquiring still have a future from a revenue and profitability perspective, especially in light of newly emerging and often cheaper payment solutions? To state this upfront: acquiring will continue to gain importance, driven by the megatrend toward digital payments and growing merchant demand for providers that can integrate and orchestrate an increasingly fragmented payments landscape. For banks in particular, acquiring will become even more strategically important as a means of creating a “walled garden.” After all, leaving one’s own corporate clients to third-party acquirers — many of which are increasingly moving into the banking business — entails significant risk. At the same time, however, the nature of value creation is fundamentally changing. Pure acceptance and processing have largely become a commodity and margins will continue to come under pressure. Instead, they should be understood as the entry point. The successful business model is shifting toward segment-specific propositions and add-ons, value-added services (VAS), and additional financial products built on top of it — all underpinned by excellent customer experience, innovation leadership, and (cost) efficiency through a homogeneous technical platform. |

Acquiring remains relevant – but the playing field is shifting

The discussion about the future of acquiring is increasingly shaped by new payment solutions, wallets, and platforms. Initiatives such as Wero, international wallets from Big Tech, and increasingly embedded payment solutions — including “invisible payments” — are fundamentally changing the strategic assessment of acquiring. In parts of this debate, the narrative suggests that acquiring is losing relevance, being reduced to a replaceable technical function and facing growing margin pressure. This impression is misleading. Even in a landscape of new infrastructures and payment rails, powerful acquiring services remain essential. As payments continue to shift away from cash and fragmentation increases due to new payment rails, acquirers will remain indispensable through their integrative and orchestrating role as well as their ability to provide highly relevant and curated data. Merchants continue to expect integrated and easily implementable solutions that bring together the growing variety of payment options, regulatory requirements, risk considerations, and reporting obligations — while also delivering data-driven insights. Through their deep integration into merchants’ operational processes—technically, commercially, and through data — acquirers have access to relevant information on payment flows, revenues, transaction frequencies, and similar metrics. These insights form the basis for well-founded risk, fraud, and credit decisions, creating a natural bridge to traditional banking products such as financing or account services. Few other business areas combine such operational proximity with comparable access to data. The role of acquiring is even more nuanced for banks. For them, the question of acquiring’s future profitability is only of secondary importance. Much more critical is the role of acquiring in creating a “walled garden”. Institutions that neglect the acceptance business open the door for third-party providers to access their corporate clients — creating an entry point for the gradual migration to additional banking products. Non-bank acquirers typically pursue a clear strategy: they perfect individual products or specific use cases, gradually build a portfolio of additional services on top of it, and thereby deepen their penetration of merchant relationships. As a result, acquiring is therefore not the end point but the platform for a broader business relationship. Based on banking licenses and rich transaction data, providers can subsequently offer merchants banking products such as financing, accounts, and cards. For banks, this implies a clear strategic reality: those who relinquish acquiring risk the long-term erosion of their corporate client relationships. |

Cheaper payments through A2A – who really “loses”?

Where, then, do the concerns about the future of acquiring originate? They are primarily driven by the anticipated expansion of alternative account-to-account (A2A) payment solutions, which are often perceived as cheaper alternatives and could therefore place further pressure on provider margins in the future. However, the assumption that A2A payments will be significantly cheaper than card-based rails is far from certain. While some cost advantages may be expected, solutions such as TWINT in Switzerland demonstrate that A2A-based systems are not necessarily substantially cheaper. Merchant service fees there — depending on industry, transaction volume, and service scope — can in some cases reach levels comparable to card payments. One reason is that a significant portion of costs is not rail-specific but arises from fraud prevention, operations, support, and compliance. A good example for this is the Electronic Direct Debit (ELV) and the Online Direct Debit procedure (OLV) used in German retail. While both represent lower-cost, account-based payment methods, OLV additionally performs real-time blacklist and credit checks. These additional services create extra costs, making OLV more expensive than ELV. At the same time, however, they significantly reduce the risk of chargebacks for the merchant. |

Overall, however, it is likely that merchants will benefit from lower-cost solutions if A2A payments achieve widespread acceptance. While this may create some margin pressure for payment providers, it can be offset elsewhere. Moreover, the more substantial structural pressure will primarily affect issuers and in particular international card schemes. In this context, A2A solutions such as Wero also serve as a strategic counterbalance.

Where Is value creation shifting?

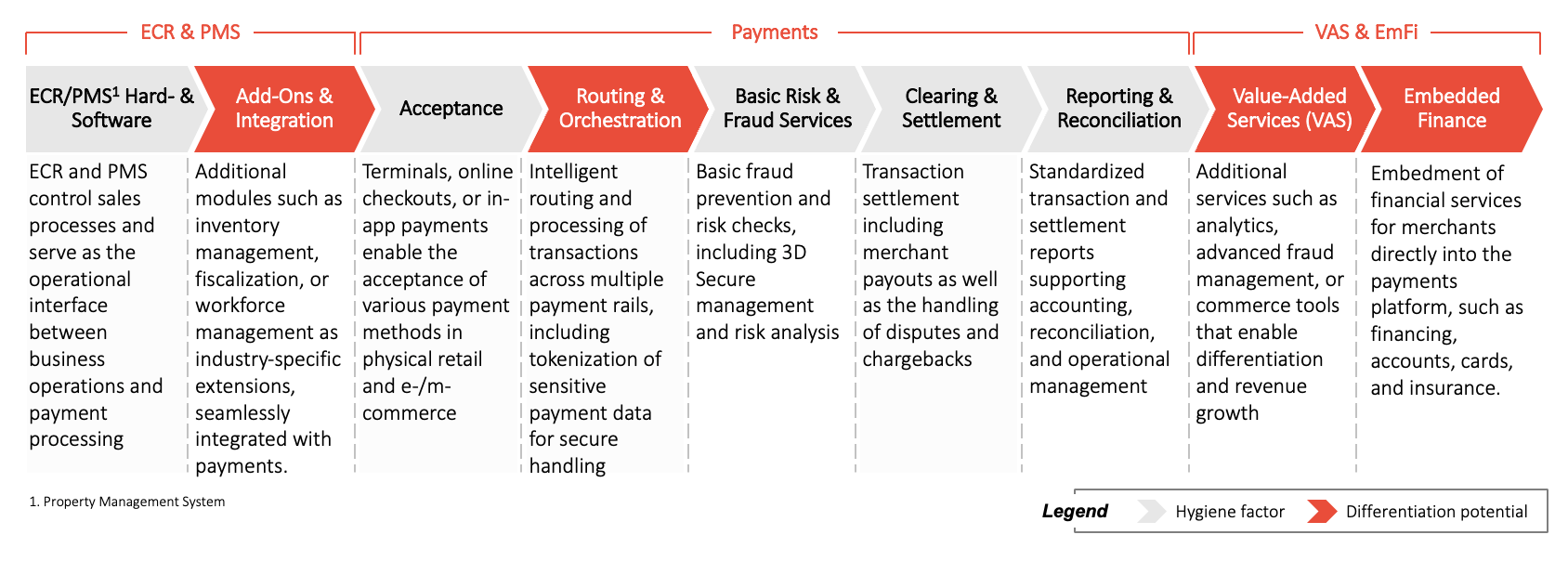

Acquiring therefore remains a critical economic function. The real structural question is not whether acquiring will continue to exist, but how monetization will take place in the future. Pure payment processing is increasingly becoming interchangeable and is subject to scale effects and price competition. The future relevance of acquiring lies less in individual rails and transactions and more in the ability to integrate and orchestrate different payment methods, make transaction data usable, and thereby strengthen customer relationships and create lasting customer lock-in. As a result, value creation is shifting to upstream and downstream parts of the value chain (see Figure 2). Key levers include segment-specific, integrated solutions with additional modules, value-added services, and bank-related products such as working-capital financing and accounts. The crucial point is not to view acquiring in isolation but as a strategic entry point that enables access to these adjacent revenue streams. |

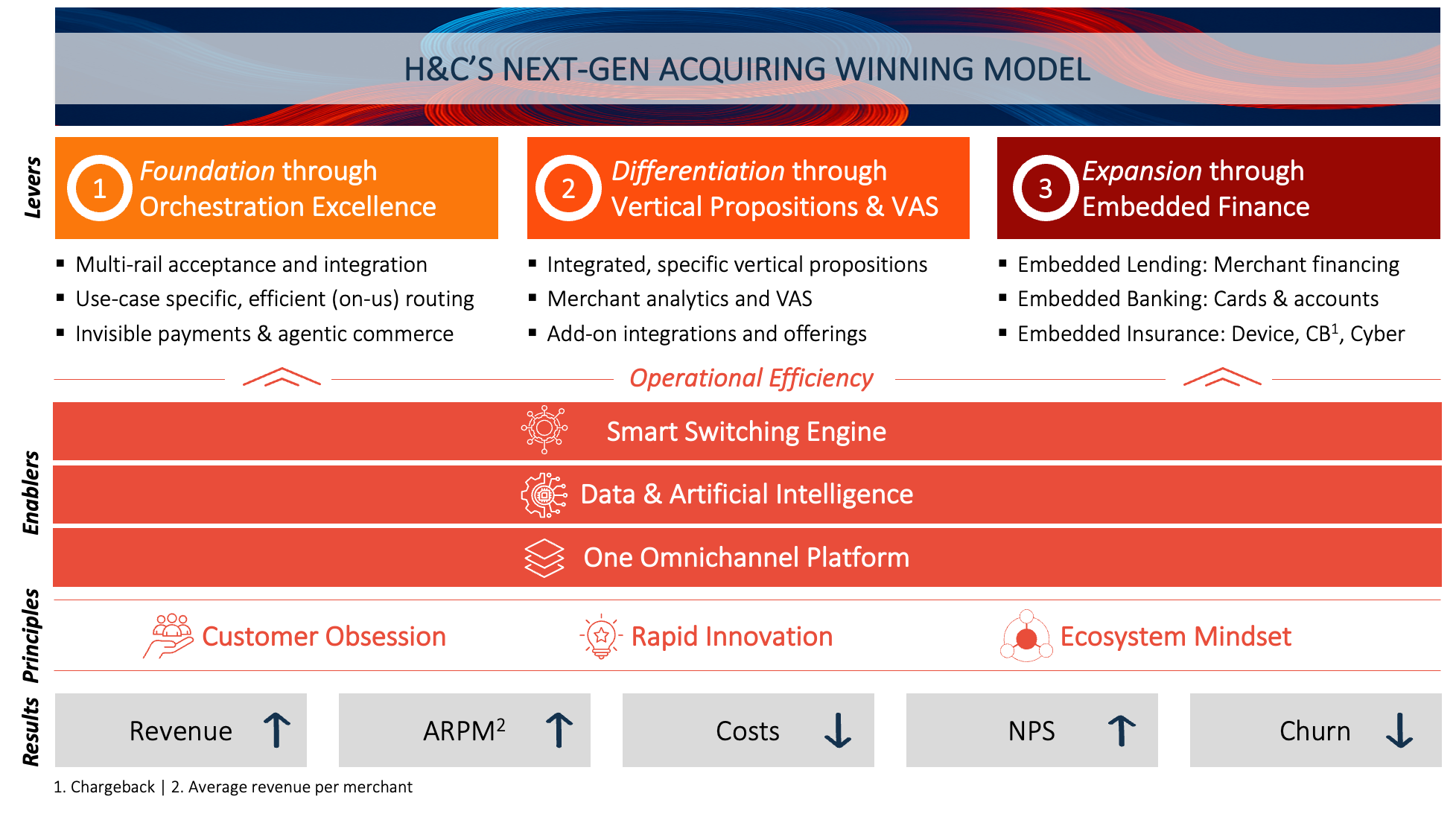

The Next-Gen Acquiring Winning Model

| In light of these fundamental changes, acquirers need to realign their business models to remain successful in the future. From our perspective, the Next-Gen Acquiring Winning Model (Figure 3) consists of three strategic levers for securing customers and revenue pools, a set of enablers that not only make these possible but also support their efficient delivery and thereby reduce costs, and a number of operating principles that form the foundation for the long-term viability of the business model. |

The three strategic levers of the new winning model

The foundation of every successful acquirer remains operational excellence and cost efficiency in processing, as these determine successful access to merchants. Merchants expect stable, high-performance, and always-available processing services — or put differently: state-of-the-art hardware including SoftPOS, maximum uptime/availability (including offline payments in various industries), low latency, fast settlement (exceptions apply), and reliable transaction handling (including refunds and disputes). At the same time, initial onboarding and ongoing customer service are expected to be fast, digital, and frictionless across channels. As the payments landscape becomes increasingly fragmented due to the growing variety of payment solutions, the integration and orchestration role of the acquirer is also gaining importance. Merchants expect their acquirer to address payment acceptance holistically — efficiently connecting different payment rails and orchestrating between them depending on the use case and cost structure, enabling excellent customer journeys, and providing consistent, comprehensive reporting and service. Smart routing — such as the enablement of “on-us” transactions — is already expected in many markets. At the same time, acquirers must prepare for the upcoming revolution of agentic commerce and position themselves accordingly. Even with excellence in these areas, however, margins are increasingly under pressure. As a result, vertically integrated industry solutions, value-added services, and banking products are becoming increasingly important. Vertically integrated industry solutions refer to tailored end-to-end solutions for specific segments — ranging from ECR systems and payment acceptance to value-added services, embedded finance, and additional integrations such as fiscalization, workforce planning, or inventory management. Examples include comprehensive solution packages for sectors such as hospitality, EV charging, or the broader unattended payments environment. Within the area of value-added services, three categories are particularly critical for success:

Leading acquirers in the market have already implemented this logic consistently. Providers such as Adyen and Stripe increasingly position themselves as comprehensive omnichannel commerce platforms that provide merchants with a wide range of operational tools in addition to payment acceptance. Payment processing thus becomes the entry point into a broader service ecosystem. The largest additional value creation lever, however, often lies one step further: embedded finance. Payment data provides unique insights into a merchant’s revenue development, liquidity, and business risks. Embedded lending primarily includes revenue-based working capital financing that can be automatically underwritten using real transaction data and repaid through daily card sales. For merchants, this provides easily accessible and quickly available financial resources, while acquirers unlock additional — often high-margin — revenue streams. Once such deep integration between acquirer and merchant has been established, the step toward embedded banking, with further offerings such as accounts or cards, is not far away. It is therefore no coincidence that an increasing number of payment providers now hold their own banking licenses. Examples such as Adyen or Viva demonstrate how providers are systematically expanding their value creation into banking areas. Embedded finance offerings can be further complemented by embedded insurance, including device insurance, chargeback insurance, or cyber insurance. |

Enablers for Next-Gen offerings and efficiency

To deploy the strategic levers effectively and cost-efficiently, a number of key enablers are required. At the center is a homogeneous omnichannel platform as the technological foundation. This platform integrates processing for physical POS as well as digital channels, orchestration, merchant management, data analytics, and value-added services in a single environment. Such an architecture makes it significantly easier to integrate new functionalities and payment methods, deliver services consistently and frictionlessly across channels, and centrally analyze data. At the same time, scale effects and cost advantages arise from consolidating previously separate system landscapes. Against the backdrop of increasing payment fragmentation, this becomes a decisive competitive advantage over market participants whose historically grown tech landscape — often the result of inorganic growth — consists of isolated systems (e.g., processing, fraud, reporting) and separate merchant portfolios. Based on this platform, consistent cross-channel data management becomes possible, enabling the targeted use of artificial intelligence. This not only creates new value-added services but also increases the efficiency of existing processes, for example in customer service or risk management. In addition, a smart switching engine should be established on top of the omnichannel platform, enabling cost-efficient, use-case-specific routing across different payment rails — including the use of “on-us” transactions. Next-Gen enablers are therefore not only prerequisites for new offerings but also key levers for improving the efficiency of existing operations. |

Operating principles for sustained success

A consistent focus on clearly defined customer segments and contexts will become a central success factor for acquirers in an increasingly competitive market characterized by agile new players and rising customer expectations. Winning individual merchants may depend on very specific requirements, such as the availability of suitable terminals, offline acceptance capabilities, or industry-specific additional services from a single provider (e.g., fiscalization). Closely linked to this is the second operating principle: fast innovation cycles. The payments market is one of the most dynamic segments of the financial industry. New payment solutions, regulatory changes, and rising merchant expectations significantly increase innovation pressure in acquiring. Successful providers are distinguished less by generating new ideas than by their ability to translate innovations quickly into scalable, market-ready solutions. The third principle is an ecosystem mindset. Successful acquirers of the future will no longer view payments as an isolated end product, but rather as the entry point into a comprehensive merchant ecosystem. Through a central integration, they provide merchants with access to a wide range of complementary services — both from their own portfolio and from third-party providers. |

Conclusion

Acquiring remains relevant — and will become even more strategically important. However, it will remain profitable and sustainable only for providers that do not view payment acceptance in isolation, but rather as a strategic entry point into an expanded commerce and finance ecosystem. In the future, margins will increasingly be generated beyond the transaction itself. For banks, acquiring has an even broader strategic significance that goes far beyond pure profitability considerations: those who control acquiring possess a central access to corporate clients. Institutions that fail to offer a competitive acquiring proposition – by itself or in select partnerships – effectively hand over a central merchant access point to third parties — along with the opportunity for those providers to gradually take over core banking products such as financing. Now is the time to reposition acquiring strategically — technologically, organizationally, and commercially. This may require difficult adjustments to established models and legacy infrastructures, but with strong execution discipline it will prepare the business model for the future. Those who postpone this sometimes painful process risk not only their margins but also losing access to the merchant relationship. |

Ready to take the next step?

Whether you have initial ideas or concrete plans, we listen, ask questions, and develop them further together. In a non-binding initial consultation, we clarify where you stand and how we can support you.