Private Banking at Cantonal Banks: How to Scale Systematically

Cantonal banks are increasingly strengthening their non-interest income business. Private banking offers significant potential, yet market conditions alone hardly explain success. We outline three building blocks that should be addressed to systematically expand the segment.

Private banking is gaining strategic relevance for cantonal banks

In the current market environment, expanding non-interest income is gaining importance for many cantonal banks. This is reflected partly in explicit strategies and partly indirectly through a stronger focus on investment expertise, advisory services, and revenue diversification. [1] [2] [3] [4]

This development is unsurprising. For many cantonal banks, interest income remains a central earnings driver. At the same time, the environment has become more challenging: in March 2026, the Swiss National Bank kept the SNB policy rate at 0%—a scenario that can be even more challenging for maturity transformation than a negative-rate environment, which banks have already learned to manage. The implication is clear: if you want to make the earnings base more resilient, it is a must to strengthen non-interest income systematically. [5]

Private banking is an obvious segment worth to consider. High-net-worth clients typically hold a higher share of securities-related assets, have more complex advisory needs, and therefore offer attractive potential for recurring commission and service income. What one should not neglect: private banking entails higher requirements in terms of advisory depth, product breadth, relationship management, steering, and risk management.

Cantonal banks have different starting positions—and leverage them differently

From an external perspective, cantonal banks’ starting positions are heterogeneous. Some differences can be explained by structural market conditions, for example taxable wealth per capita in the respective canton. The intuitive hypothesis is: the higher the unrestricted taxable wealth per capita, the more favourable the starting position for a cantonal bank’s private banking business.

As an external success metric, securities-related income can be used. While this is only a rough proxy for private banking (among other things, depending on the bank it may include contributions from other segments), it is disclosed across all cantonal banks and can therefore be used as a “back-of-the-envelope” indicator.

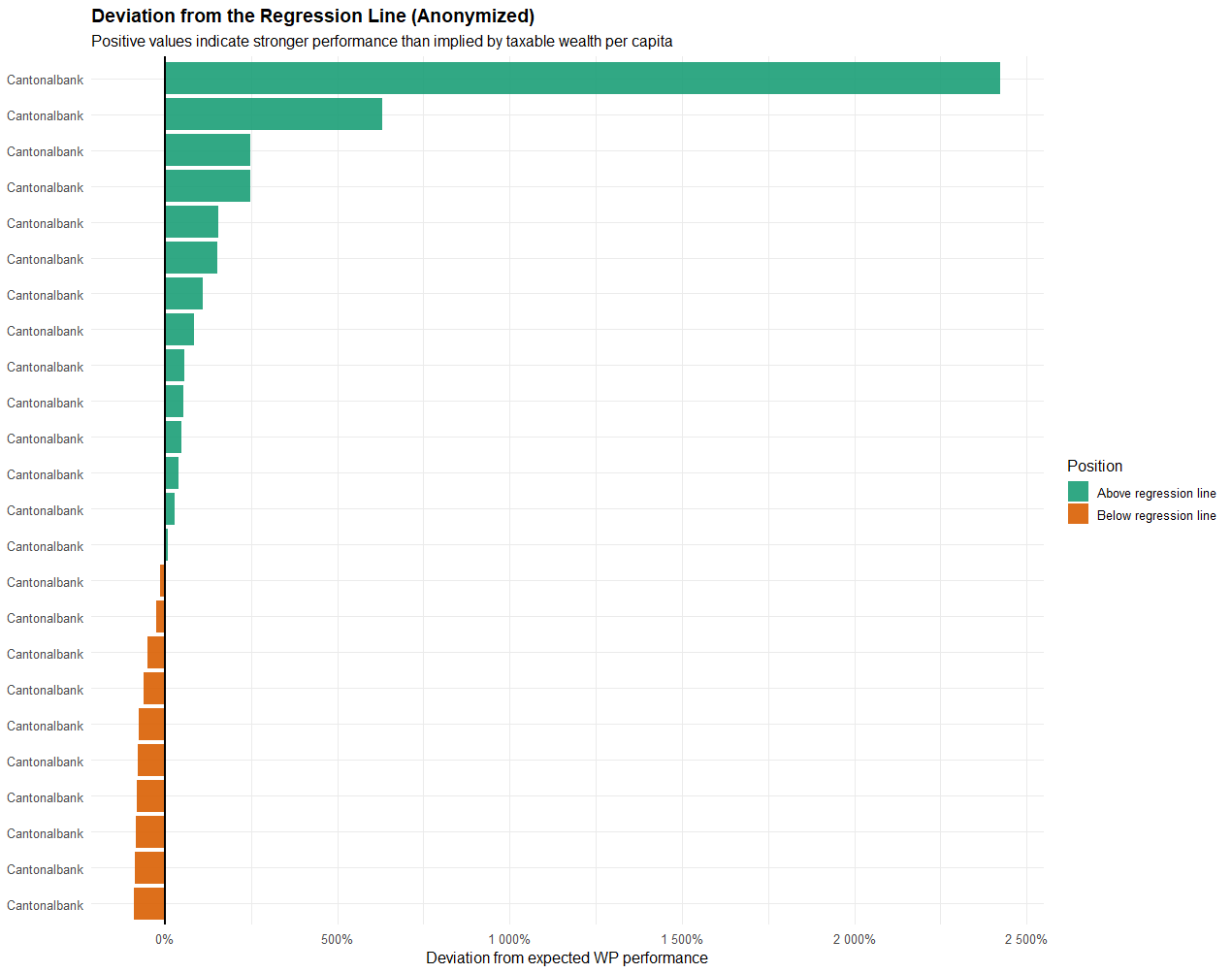

Based on our dataset (ESTV-data as of 2022 wealth-statistic; securities-related income: H1-2025 (latest complete set)), some banks deviate very significantly on the upside from the expected value (in the log model, the strongest positive deviation is around 2,400%). At the same time, an R² of roughly 0.001 also shows: the tax base alone explains virtually none of the differences in securities-related income.

The right conclusion is not that market structure is irrelevant—quite the opposite. Cantonal banks start from different conditions. But the real performance delta arises from the ability to translate potential into profitable client relationships, mandates, and recurring revenues. Some of the banks seem to be very successful in excavating the market-situation (positive difference) while others lag behind.

Given the current landscape marked by renewed uncertainty, cantonal banks’ structural set-up—particularly with regard to the safety of assets (21 of the 24 cantonal banks benefit from a form of guarantee that goes beyond deposit protection of CHF 100k per person)—represents a compelling positioning for wealthy clients.

How to scale the segment systematically using three building blocks

Based on our project experience, three building blocks are decisive for systematically expanding private banking:

|

1. Precise assessment of the starting position & target definition

The first building block is a robust baseline assessment. This requires analysing both internal capabilities and the concrete market situation. On the bank side, three questions are particularly important:

Ultimately, it is the organisation and its specific capabilities that determine value creation in private banking. Accordingly, the relevant levers should be explicitly considered in the assessment. We recommend focusing on the following themes:

At the same time, the market situation must be assessed in a differentiated way. Depending on the canton, wealth structure, competitive intensity, inflow dynamics, density of entrepreneurs, or the relevance of internationally mobile professionals can differ significantly. The result is not a “standard strategy,” but a bank-specific opportunity profile. On this basis, target customers must be defined cleanly. In practice, concrete personas work much better than abstract segment labels—because only if it is clear which customer types are being addressed can advisory approach, offering, and go-to-market be aligned consistently. |

2. Tailored derivation of product portfolio, distribution channels and networks

After defining target customers, the product portfolio and distribution approach must be derived. First, it should be assessed critically whether the existing portfolio truly meets target customers’ needs. In private banking, an expanded standard retail offering is often insufficient. What is required are robust solutions in discretionary mandates, advisory, pension planning, succession, and structuring. A recurring pattern in projects is the growing relevance of intergenerational advice. Anyone aiming to manage wealth over the long term must understand not only the current asset allocation, but also transitions between wealth accumulation, wealth preservation, and wealth transfer. This has direct implications for product architecture, coverage model, and the qualification of advisors. Equally important is the choice of distribution channels. Private banking rarely emerges from classic lead generation alone. Successful models often connect retail, corporate banking, pensions, entrepreneur business, and external networks in an intelligent way. Cantonal banks with strong regional roots have a structural advantage here—provided they make it organisationally actionable. They make this fundamentally favourable positioning actionable, on the one hand, through systemic / networked thinking with other organisations to create added value for (potential) clients; and on the other hand, through leveraging networks for new client acquisition as well as targeted campaign steering. Implementation is not only an operational topic, but also a cultural one. Expectations in private banking differ fundamentally from retail: less transaction, more relationship; less standardisation, greater advisory depth; less product selling, more trust-building. Accordingly, advisors must be developed and supported deliberately, and equipped with the right tools. |

3. Establishing effective, aligned controlling

The third building block is a controlling approach that fits the business model. Many institutions still steer the segment too heavily via closures or volume metrics, and too little via the economic quality of the client relationship.

The first lever lies in the “as-is”: a systematic analysis of the current steering logic often reveals substantial potential. A practical example is the handling of special conditions. In many organisations, there is no consolidated view of where, why, and with what earnings effect pricing concessions are granted. Especially in private banking, this is a direct earnings driver and therefore an obvious starting point for short-term improvement.

In addition, forward-looking performance controlling is required. Isolated product sales are too narrow in private banking. What matters is the economic value of the entire relationship over time. Accordingly, metrics such as Customer Lifetime Value, wallet share, mandate penetration, and coverage intensity gain importance.

Another often underestimated aspect is the network value of a relationship. If a client facilitates access to additional high-quality relationships, acquisition costs decrease and revenue potential increases. This value should also be reflected in steering—at least qualitatively, and ideally quantitatively.

Finally, private banking is not static. Market conditions, client expectations, and competitive intensity evolve continuously. Accordingly, the key levers—from product breadth and pricing power to advisory quality—must be measured and recalibrated on an ongoing basis. Sustainable success does not come from a one-off strategic decision, but from consistent steering.

How Horn & Company can support

We bring our expertise across all areas required to build a successful path to expanding the private banking segment. Our objective is to strengthen your go-to-market effectiveness and generate a measurable return on consulting. We combine deep market understanding of Switzerland with comprehensive methodological expertise. Accordingly, we are happy to support in any situation—whether on a single building block or in developing the full set of building blocks for the targeted expansion of the private banking segment.

Ready to take the next step?

Whether you’re just starting to think about it or have concrete plans — we’ll listen, ask questions, and work with you to develop your ideas further. In a no-obligation initial consultation, we’ll assess where you stand and how we can support you.

Sources

[1] https://www.lukb.ch/ueber-uns/medien/news/strategie-lukb30

[2] https://www.zkb.ch/de/ueber-uns/unser-unternehmen/konzernstrategie.html

[3] https://www.bkb.ch/de/die-basler-kantonalbank/medien/medienmitteilungen/2025/die-strategie-2026-des-konzerns-bkb-fokussiert-auf-vertriebsexzellenz-anlagekompetenz-bilanzmanageme

[4] https://www.bekb.ch/die-bekb/publikationen/medienmitteilungen/2026/20260129-bekb-jahresabschluss_2025

[5] https://www.snb.ch/de/publications/communication/press-releases-restricted/pre_20251211