Fields of action for efficient overall bank management

The new dynamics of the interest rate curve following the prolonged low interest rate phase have exposed weaknesses in the interest rate book management of many institutions: an overly aggressive maturity transformation is having a lasting negative impact on earnings – even after the “reversal of the reversal.” Increased market volatility is driving a greater need for flexible and dynamic management approaches to interest income – but also for ensuring liquidity.

At the same time, regulatory pressure is mounting: With the introduction of CRR III and, in particular, the planned output floors, RWA burdens are increasing significantly. Combined with rising capital costs, efficient capital and RWA management is moving further into focus. Given the multitude of regulatory requirements and the constant stream of implementation projects, many institutions are left with few resources for a business management perspective on overall bank steering. However: integrated bank management (GBS) is more than just a regulatory obligation – it is a key lever for sustainable banking success.

“We view modern integrated bank management as an efficiency lever for optimizing risk-adjusted value contributions from a bank’s resource utilization.”

Now more than ever, it is worthwhile to take a close look at this efficiency potential.

Operation Model of an integrated overall bank Management

An effective integrated bank management (GBS) requires close coordination between Treasury, Risk Management, and Controlling – and thus between the 1st and 2nd Line of Defense.

An integrated GBS combines earnings and risk perspectives along clearly defined responsibilities in order to avoid conflicts of interest and to proactively assess market movements together: Where are the risks – and where are the opportunities?

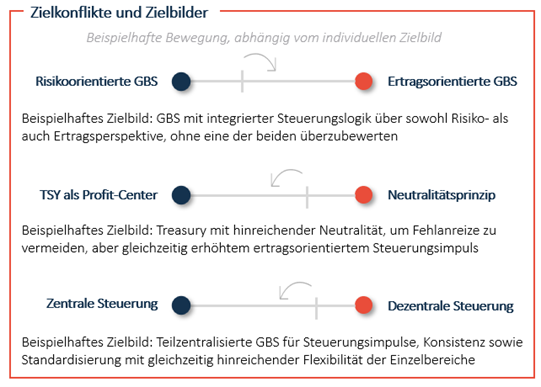

The organizational cornerstone of GBS is the Asset-Liability Committee (ALCO) or comparable committees. It functions as the central steering body and orchestrates the collaboration of the GBS functions along their specific areas of responsibility. Strategically, the focus is placed on transparency in the delineation of risk and earnings, the use of risk-adjusted performance measures, and closely coordinated planning: medium-term planning, ICAAP, and ILAAP connect top-down requirements with bottom-up needs in order to integrate the demands of the “internal banking customers” in a targeted manner. By linking the risk and earnings perspectives, GBS is continuously subject to a series of goal conflicts, for which a viable compromise must be found again and again.

An effective integrated bank management (GBS) is characterized by structural clarity, role-based accountability, and an integrated steering approach – with the goal of not only fulfilling regulatory requirements but actively shaping the bank’s future viability.

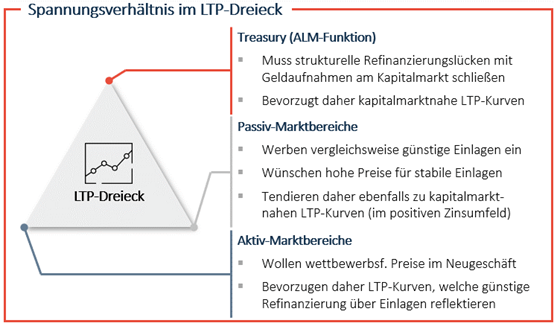

Liquidity Transfer Pricing as the Nervous System of Integrated Bank Management

An effective LTP system enables a causality-based allocation of provided and utilized liquidity within an institution. As a best practice, liquidity is charged using maturity-matched pricing through appropriate LTP curves – meaning: liquidity is priced in accordance with how it is actually used in terms of maturity, volume, and structure.

The LTP system lies at the heart of diverging interests within the institution:

Due to the tensions illustrated in the diagram, an LTP system in practice is always a management-effective compromise rather than a purely theoretical optimal solution.

Acceptance of LTP systems is often not consistent – in particular, front-office business areas frequently question the LTP logic, for example due to concerns about potential earnings losses or lack of steering relevance.

An LTP system can only be effective if it is supported by all involved areas.

The goal is to design viable, balanced compromises within the LTP triangle that unite operational reality and strategic management.

Durch die im Schaubild dargestellten Spannungen, ist ein LTP-System in der Praxis stets ein steuerungswirksamer Kompromiss, nicht die rein theoretische Optimal-Lösung.

Die Akzeptanz von LTP-Systemen ist häufig nicht durchgängig gegeben – insbesondere Aktiv-Marktbereiche stellen die LTP-Logik oft infrage, etwa wegen befürchteter Ertragseinbußen oder mangelnder Steuerungsnähe.

Ein LTP-System kann nur wirksam sein, wenn es von allen beteiligten Bereichen getragen wird. Es gilt, tragfähige, balancierte Kompromisse innerhalb des LTP-Dreiecks zu gestalten, die operative Realität und strategische Steuerung vereinen.

Implicit options in the interest rate book – particularly contractually agreed or legally anchored termination rights such as those under § 489 of the German Civil Code (BGB) – are becoming significantly more important in a volatile interest rate environment.

These rights enable customers to terminate long-term loan agreements early, for example to benefit from more favorable conditions. As a result, hidden burdens arise for the institution, which negatively affect the net interest income if exercised rationally. Comparison portals and increased customer awareness can reinforce this rational exercise behavior – the risks then materialize more frequently and noticeably.

Implicit options thus represent a direct risk to the long-term earnings value of the interest rate book.

Especially in a present value-oriented perspective, implicit options can further distort steering signals and thereby also pose an indirect risk to long-term earnings value. Often, there is a lack of sufficiently long historical data for adequate calibration of risk models. Instead, consistent management is required that creates transparency regarding the nature, scope, and impact of the implicit options.

A central success factor is the close integration of valuation and modeling, operational steering, and transaction processing.

Valuation and modeling require realistic assumptions about customer behavior and exercise probabilities. In operational steering, measures such as hedging and adjusted margin calculations are needed, while the back office must be able to process the resulting hedging transactions.

Implicit options are no longer a theoretical fringe issue.

They have a direct impact on net interest income – often unnoticed, but effective. In a volatile interest rate landscape, the ability to manage them determines whether they contribute to value or result in loss.

strucural liquidity as an independent GBS-management Field

Beyond the classic interest rate book, structural liquidity carries its own earnings and risk potentials.

Analogous to interest rate fixation cash flows, capital commitment cash flows reflect the maturity structure of structural liquidity. In contrast to its “big brother” – interest rate book management – the use of derivative steering instruments must be avoided in practice when managing structural liquidity. At the same time, future refinancing costs and benefits can be actively managed. Structural liquidity is treated consistently with the LTP system – for example, by making it controllable via a separate LTP book. The basis for this is a robust refinancing plan that enables active management in normal phases.

The management concept should be methodologically aligned with adjacent steering areas, particularly interest rate book management and CSRBB steering. The goal is to avoid contradictory signals regarding margins and margin risks, as well as double counting of spread risks.

At the short end, structural liquidity is constrained by short-term liquidity risk, since maturity mismatches at the short end must always be covered. In the medium-term range, it is primarily affected by regulatory requirements such as the NSFR in the first maturity band of one year. Beyond that, however, it largely remains unregulated – which opens up economic room for maneuver.

In many institutions, structural liquidity has not yet been established as an independent management area.

As a result, value contributions and risks often remain untapped or hidden.

Conclusion: Rethinking integrated bank management – integrated, dynamic, effective

The current challenges in the interest rate, capital, and liquidity environment clearly show:

Modern integrated bank management must go far beyond merely fulfilling regulatory requirements.

It is both a strategic efficiency lever and an operational steering instrument.

Those who think of GBS holistically today and anchor it consistently in operations unlock sustainable sources of income, reduce hidden risks – and thereby strengthen the future viability of the bank in an increasingly volatile environment.

Ready, to take the next step?

Whether initial thoughts or concrete plans – we listen, ask questions, and develop ideas further together.

In a non-binding initial consultation, we clarify where you currently stand and how we can support you.

Set up a meeting now!