How to tackle the delegated authorities (DA) opportunity in Europe

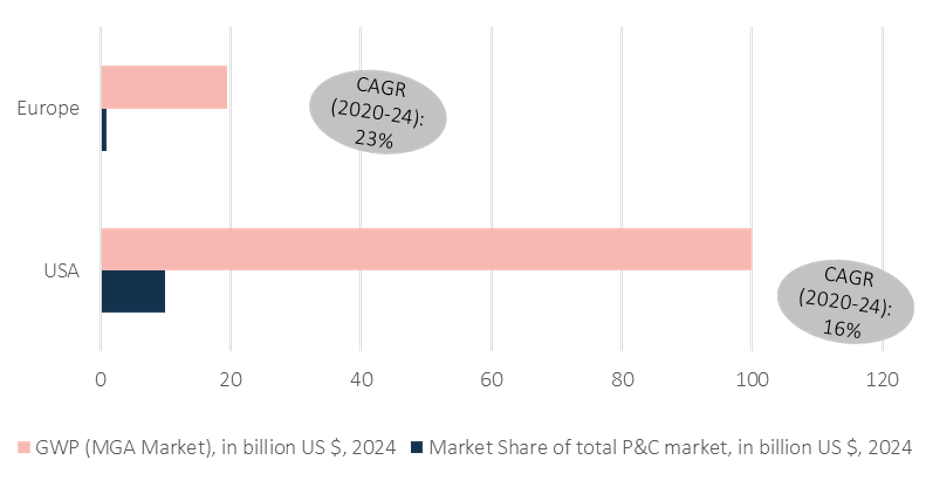

Delegated authority and the Managing General Agent model have moved from being niche distribution constructs to becoming strategically relevant pillars of the global insurance industry. While the United States continues to represent the most mature and established MGA ecosystem, the European market has recently entered a phase of accelerated expansion. The founding of the European interest group FASE marks a turning point for the importance of DA in Europe and will ensure a stronger position and greater visibility in the future, particularly regarding insurers and regulators. Figures 1a/b show a smaller market share in Europe compared to the USA, yet a compound annual growth rate of 23 percent in gross written premium thereby surpassing growth levels in the USA. This also results in a growing number of MGAs in Europe.

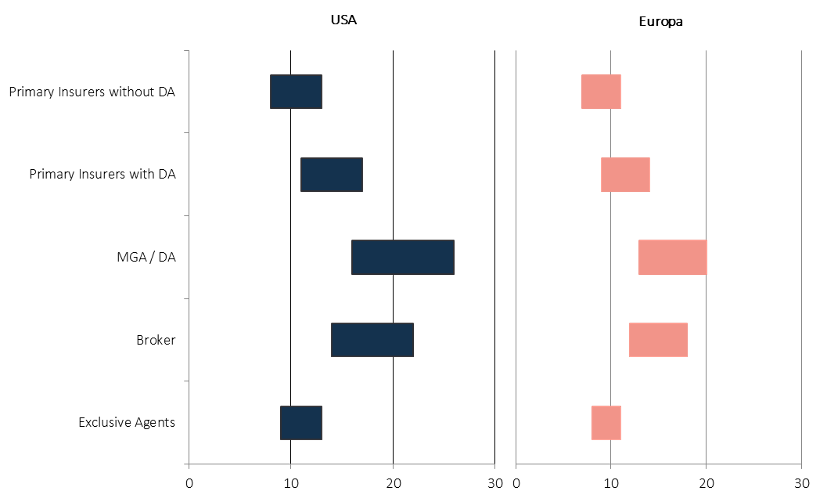

This dynamic has reinforced the MGA model’s appeal to investors and insurers alike. In the US - where InsurTech-driven MGAs and strong private-equity participation have shaped the market - valuation ranges are especially elevated, as Figure 2 shows. MGAs typically command the highest valuation multiples across the insurance value chain, driven by their asset-light structures, specialized underwriting capabilities and scalability. DA therefore ranks ahead of brokers and exclusive agents. On the part of primary insurers, there is a clear advantage if an affiliated DA already exists. As a standalone business model, DA seem more attractive than comparable plays in the industry. But primary insurers need to clarify how they can benefit from this trend.

Insurers must detail the conditions under which delegated authority constitutes a profitable and strategically sound partnership. We see that insurers already apply rigorous screening before allocating capacity, reflecting the need to safeguard underwriting profitability and alignment with risk appetite. Unlike equity investors, insurers are not evaluating MGAs primarily as financial assets but as risk-bearing extensions of their own underwriting operations. The quality, transparency and discipline of an MGA’s underwriting processes therefore directly shape the economic viability of a DA arrangement.

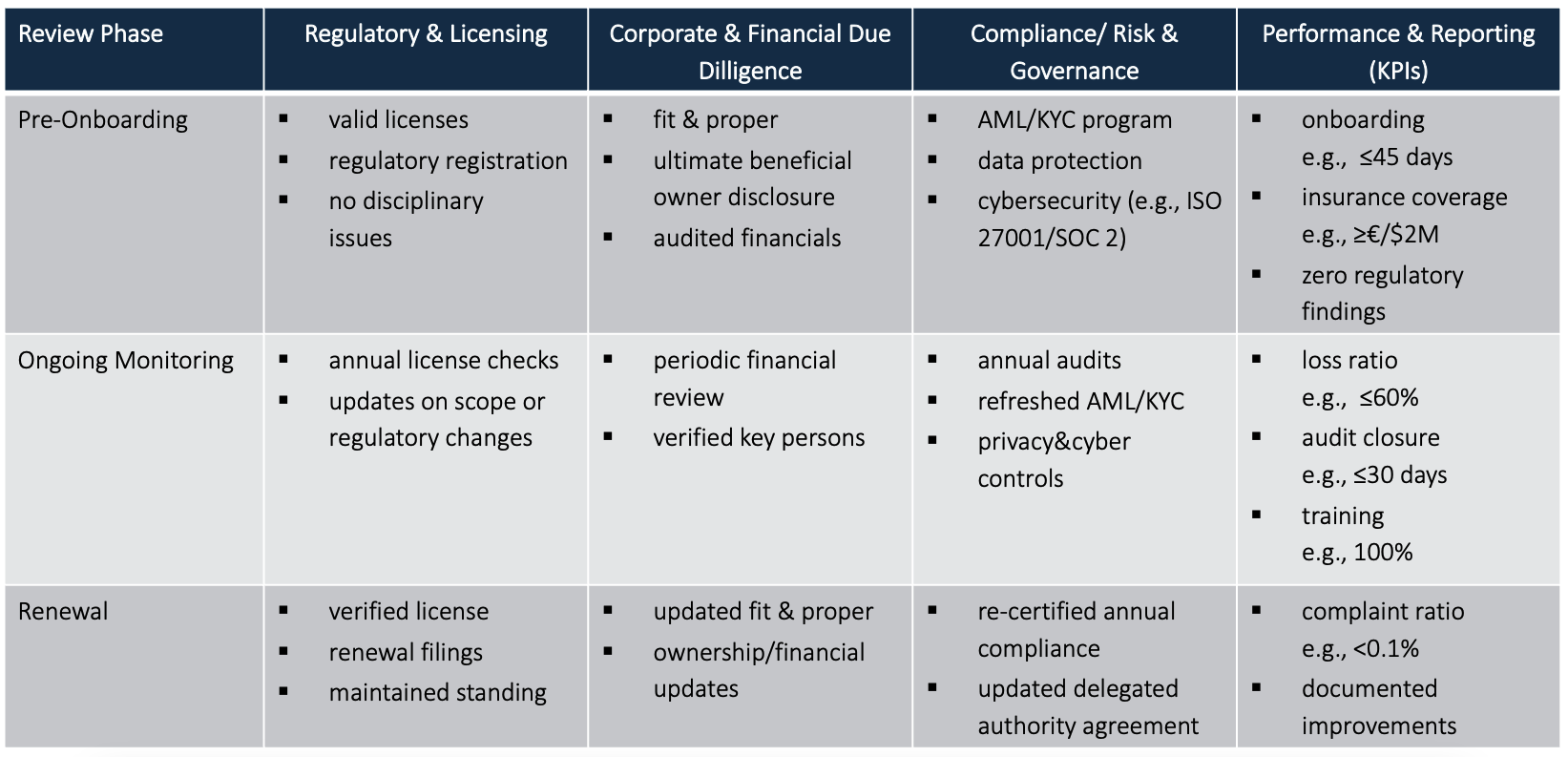

A structured and multidimensional screening process is therefore essential. We have distilled a comprehensive assessment framework leveraging four pillars: Regulatory & Licensing, Corporate & Financial Due Diligence, Compliance/Risk & Governance, and Performance & Reporting (see table 1). Disciplined monitoring along these pillars allows best-in-class primary insurers to form a holistic view on risk and performance. Such rigor is indispensable because delegated underwriting inherently introduces information asymmetry, reliance on remote operational controls, and the need for systematic monitoring of portfolio quality over time.

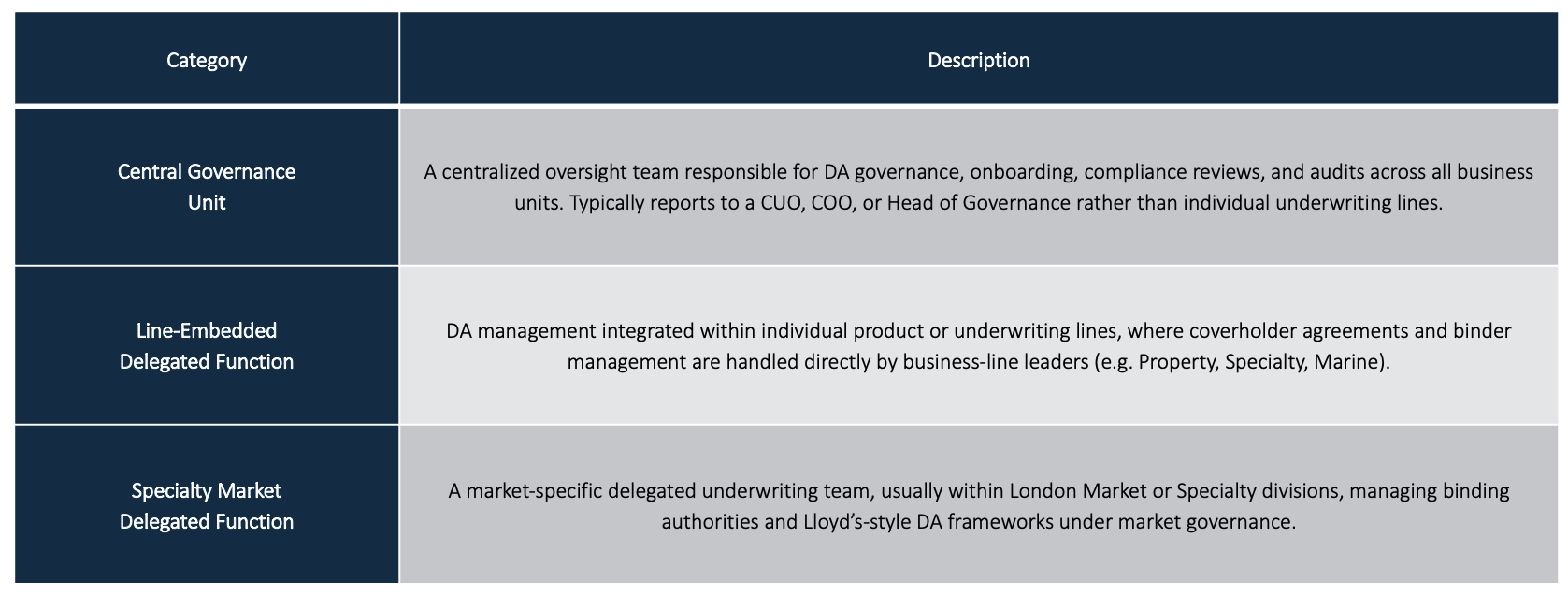

Effective governance ultimately determines whether DA partnerships generate sustainable economic value. In general, insurers must consider how they can organize DA to position themselves with the regulator and adhere to compliance requirements. When it comes to design governance, there are a number of issues to consider, in particular how to deal with complexity and interfaces, organizational embedding, and how to proceed with further scaling or, if necessary, run-off cases. We find that leading insurers in the DA industry fall into one of three archetypes (see table 2).

These governance archetypes illustrate how insurers align strategic decision-making and operational guidance into a coherent oversight system. Strong governance typically involves clear capacity allocation principles, well-defined authority limits, standardized reporting requirements, regular performance reviews and independent audit functions. These elements create both transparency and control - conditions that are indispensable in an outsourcing-intensive model such as delegated authority. However, in the market, we see a certain tendency to design DA as a separate business model with independent governance.

Several further questions are also relevant when promoting DA, e.g., the effects on accounting/finance, data models, and data analytics, etc. However, taken together, the evidence suggests that Europe is entering a new phase in the evolution of its MGA market - one characterized not only by growth but by increased institutionalization. For primary insurers, this development presents a compelling opportunity to expand specialized underwriting capabilities and access new customer and product segments. However, capturing this opportunity requires a disciplined approach: rigorous screening, a deep understanding of jurisdictional differences and a governance model that ensures accountability, data quality and underwriting integrity. Insurers that can combine these elements will be well positioned to benefit from the continued rise of delegated authority in Europe and to shape the emerging competitive landscape of this fast-evolving segment.

Ready to take the next step?

Whether you have initial ideas or concrete plans, we listen, ask questions, and develop them further together. In a non-binding initial consultation, we clarify where you stand and how we can support you.